|

| Source: Bosler, Daly, and Nechio (2014), Figure 2 |

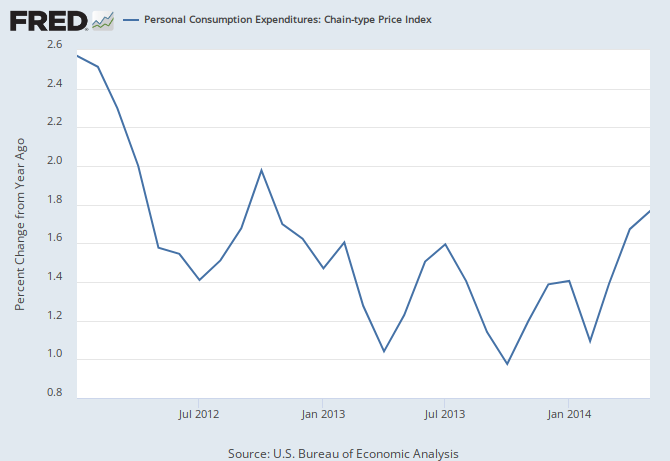

Suppose it is May and the Fed is deciding whether to increase the target rate by 25 basis points. Assume inflation is still at or slightly below 2%, and the Fed would like to tighten monetary policy if and only if the "true" state of the labor market x is sufficiently high, say above some threshold X. The Fed does not observe x but has some very noisy signals about it. They think there is about a fifty-fifty chance that x is above X, so it is not at all obvious whether tightening is appropriate. There are four possible scenarios:

- The Fed does not increase the target rate, and it turns out that x>X.

- The Fed does not increase the target rate, and it turns out that x<X.

- The Fed does increase the target rate, and it turns out that x>X.

- The Fed does increase the target rate, and it turns out that x>X.

Cases (2) and (3) are great. In case (2), the Fed did not tighten when tightening was not appropriate, and in case (3), the Fed tightened when tightening was appropriate. Cases (1) and (4) are "mistakes." In case (1), the Fed should have tightened but did not, and in case (4), the Fed should not have tightened but did. Which is worse?

If we think just about immediate or short-run impacts, case (1) might mean inflation goes higher than the Fed wants and x goes even higher above X; case (4) might mean unemployment goes higher than the Fed wants and x falls even further below X. Maybe you have an opinion on which of those short-run outcomes is worse, or maybe not. But the bigger difference between the outcomes comes when you think about the Fed's options at its subsequent meeting. In case (1), the Fed could choose how much they want to raise rates to restrain inflation. In case (4), the Fed could keep rates constant or reverse the previous meeting's rate increase.

In case (4), neither option is good. Keeping the target at 25 basis points is too restrictive. Labor market conditions were bad to begin with and keeping policy tight will make them worse. But reversing the rate increase is a non-starter. The markets expect that after the first rate increase, rates will continue on an upward trend, as in previous tightening episodes. Reversing the rate increase would cause financial market turmoil, damage credibility, and require policymakers to admit that they were wrong. Case (1) is much more attractive. I think any concern that inflation could take off and get out of control is unwarranted. In the space between two FOMC meetings, even if inflation were to rise above target, inflation expectations are not likely to rise too far. The Fed could easily restrain expectations at the next meeting by raising rates as aggressively as needed.

So going back to the four possible scenarios, (2) and (3) are good, and (4) is much worse than (1). If the Fed raises rates, scenarios (3) and (4) are about equally likely. If the Fed holds rates constant, (1) and (2) are about equally likely. Thus, holding rates constant under high uncertainty about the state of the labor market is a better option than potentially raising rates too soon.

{kind=link}